Understanding the Basics of Cost Basis

Learn the definition of cost basis. Cost basis is the original value of an asset, such as stocks, bond, mutual funds. You begin with the original purchase price, and then you adjust it for commissions, stock splits, dividends, return of capital or any other transaction that affects the original value of the asset. Once you know the cost basis, you can compare it to the amount for which you sold the asset in order to calculate capital gains or losses. You need to know capital gains for tax purposes. It is also known as the tax basis.

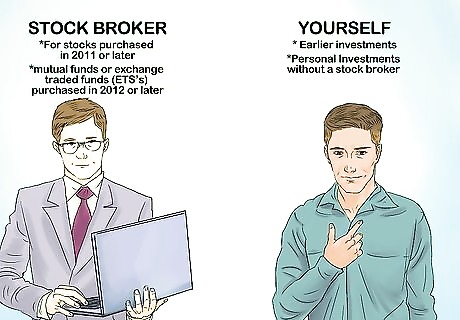

Know who calculates the cost basis. The cost basis is calculated by your stockbroker or mutual fund company for stocks purchased after 2011 or mutual funds purchased after 2012. If you invest without a stock broker, you will need to calculate the cost basis of your assets yourself in order to do your taxes. For stocks purchased in 2011 or later and mutual funds or exchange traded funds (ETS’s) purchase in 2012 or later, the stock broker or mutual fund company is required to calculate the cost basis and report it to the IRS. For earlier investments, you will need to do the calculation yourself and keep the information for your tax records.

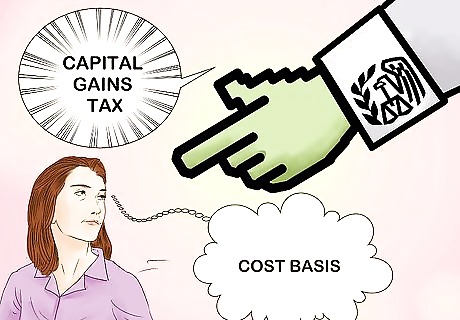

Understand why you need to calculate the cost basis. If you sell stocks, bonds or other assets, you will have a gain or loss. The Internal Revenue Service (IRS) mandates that you report all capital gains and losses on your annual income tax return. In order to accurately calculate the amount of the gain or loss, you first need to know the original starting value of the asset. This is the cost basis.

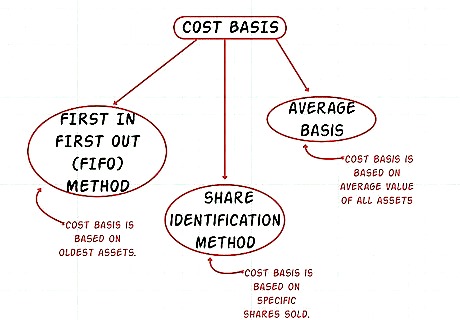

Understand the three methods for calculating the cost basis. The IRS provides different methods of calculating cost basis depending on the type of asset. For mutual funds and other equities, there are up to eight different kinds of cost basis accounting methods. The most common include first in first out (oldest shares sold first), last in first out (newest shares sold first), high cost first out, low cost first out, and the average cost method. The more detailed methods result in more accurate calculations, which may affect the amount you end up paying in taxes. You can work with your broker or mutual fund company to choose which method you want them to use to calculate the cost basis of your assets. The first method is the first in, first out (FIFO) method. This assumes that when you sell, you will sell your oldest assets first. So the cost basis is based on your oldest assets. The second method is the specific share identification method. In this method, the cost basis is calculated based on the specific shares you sold. The third method is the average basis. In this method, the cost basis is calculated based on the average value of all of your assets.

Using the First In First Out (FIFO) Method

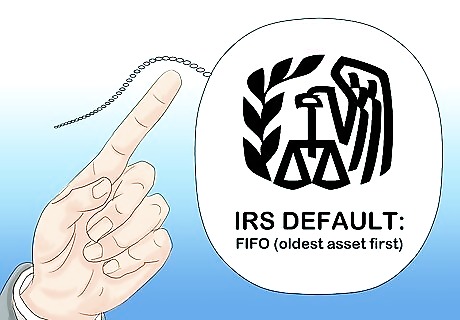

Understand the definition of the FIFO method. For this calculation, you would assume that any profit or loss you earned this year came from the sale of securities purchased first. It is the default method for calculating cost basis. Unless you specify otherwise, the IRS assumes that you used this method to calculate the cost basis.

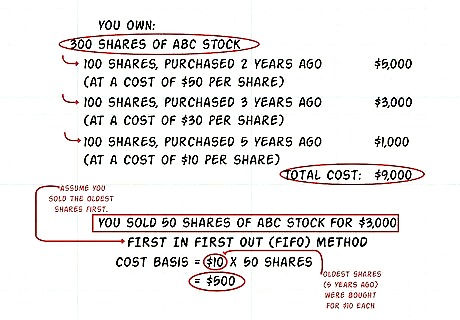

Calculate the cost basis using the FIFO method. For example, suppose you own 100 shares of ABC common stock that you purchased 2 years ago for $5,000 (at a cost of $50 per share) and 100 shares that you purchased 3 years ago for $3,000 (at a cost of $30 per share) and 100 shares that your purchased 5 years ago for $1,000 (at a cost of $10 per share). Your total holding at this point was 300 shares of ABC for a total cost of $9,000.This year you sold 50 shares of stock for $3,000. Using the FIFO method, you would assume that you sold the oldest shares first. This means you sold the 50 shares of the securities purchased initially for a cost of $10.00 per share or $500 total ($10 x 50 shares).

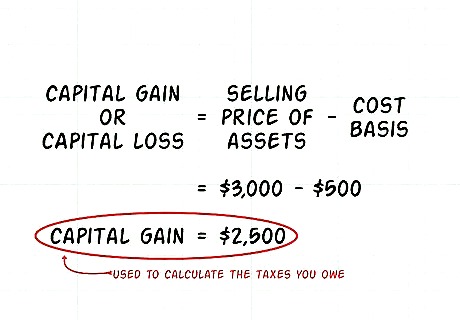

Calculate your capital gain or loss. To calculate your capital gain or loss, you subtract the cost basis from the selling price of the assets. The difference is your gain or loss. This is the amount used to figure your taxes on the sale. In the above example, the cost basis of the 50 shares sold is $500. The selling price was $3,000. Calculate the capital gain with the equation $3,000 - $500 = $2,500. Your capital gain in this example is $2,500. This is the amount used to calculate the taxes you owe.

Consider the benefits. This method is easy to understand. The assumption is simple, that the shares are sold in the same order in which they were bought. It is also uncomplicated for record-keeping. You don’t have to worry about identifying specific shares you’ve sold and figuring out the cost basis for each. However, you do need to keep good records of the different purchase dates, as the transaction date also affects whether the gain or loss is long term or short term.

Understand the drawbacks. The FIFO method is less tax-efficient. Your gains or losses are not being calculated in the most accurate way. If you want to minimize your gains or maximize your losses to offset your gains, this is not the best method to use. You have no control over which assets are used to calculate your capital gain or loss.

Using the Average Cost Method

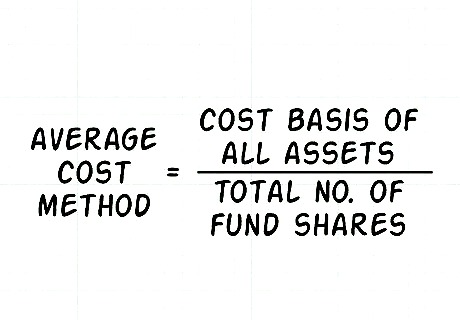

Understand the average cost method. This method is typically used for mutual fund accounts. This method adds up the cost basis for all of your assets and divides it by your total number of fund shares to calculate an average cost basis.

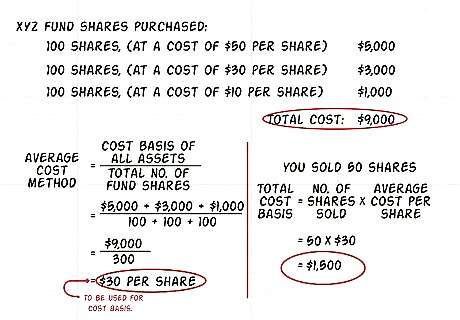

Calculate the cost basis using the average cost method. Suppose you purchased 100 XYZ fund shares for $5,000 ($50 per share), 100 fund shares for $3,000 ($30 per share) and 100 fund shares for $1,000 ($10 per share). This year you sold 50 XYZ shares for $3,000. Total the cost for all of the XYZ fund shares ($5,000 + $3,000 + $1,000 = $9,000). Add up the total number of shares (100 + 100 + 100 = 300). Calculate the average cost per share ($9,000 / 300 = $30). The average cost per share is $30. You will use $30 per share for your cost basis. Since you sold 50 shares, you multiply the cost basis per share by 50 to calculate the total cost basis (50 x $30 = $1,500).

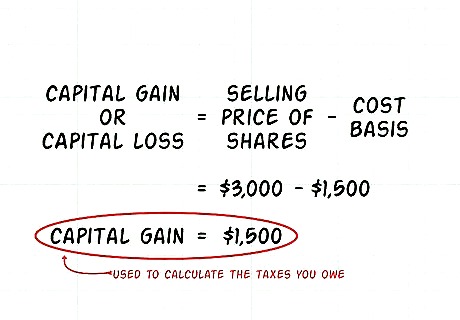

Calculate your capital gain or loss. Subtract your cost basis for the 50 shares from the selling price for the 50 shares. The difference will be your capital gain or loss. This gain or loss is used for your taxes. You sold the 50 shares for $3,000. Subtract to get the difference using the equation $3,000 - $1,500 = $1,500. Your capital gain in this example is $1,500.

Consider the benefits. Your gains and losses are spread evenly across all of the shares you own. It’s also easy to use since the calculation of the average cost is automated. This method involves little record-keeping. Your mutual fund house or stock broker can easily do the calculation for you.

Understand the drawbacks. You don’t have as much control over how much of a gain or loss is reported to the IRS for taxes. Because your gains and losses are spread evenly across all the assets you own, you can’t hand select which shares to include in the calculation. Also, this method is tax inefficient. Since the same cost basis is used for all of your assets, you can’t maximize gains or minimize losses for tax purposes.

Using the Specific Share Identification Method

Understand the definition of the specific share identification method. In this method, you identify specifically which shares were sold. You find out the cost basis, or original cost, for each of these shares, and calculate the loss or gain accordingly. This requires the most record-keeping, but it allows for very accurate tax information.

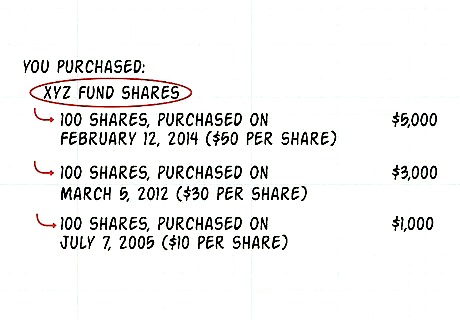

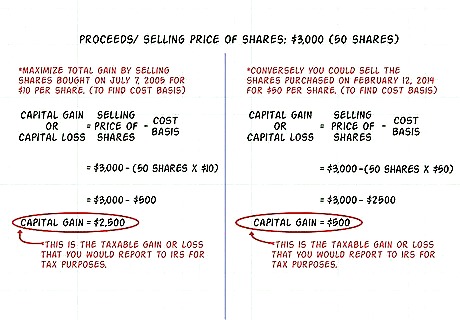

Calculate the cost basis using the specific share identification method. Suppose you had purchased 100 XYZ fund shares on February 12, 2014 for $5000 ($50 per share), an additional 100 shares of XYZ on March 5, 2012 for $3,000 ($30 per share), and a third 100 shares on July 7, 2005 for $1000 ($10 per share).

Calculate your capital loss or gain. Subtract the cost basis of the shares from the selling price. The difference is your taxable gain or loss. This is the amount you would report to the IRS for tax purposes. The specific share identification method allows you the freedom to select which of the shares you hold in your portfolio to sell. To maximize your total gain, you would sell the shares purchased on July 7, 2005 for $10 per share. The cost basis of the shares would be $500 (50 x $10). The proceeds of the two sales would be $3,000. As a consequence of your selection, you would report a $2,500 capital gain. Conversely, you could select to sell the shares purchased on February 12, 2014 for $50 per share. Your cost basis would be $2500 (50 shares x $50 per share). Since your proceeds are $3,000, your capital gain would be $500 ($3,000 - $2500).

Consider the benefits. This method gives you more control because you can choose the most advantageous shares to sell. It also makes your tax bill more accurate, and potentially lower than the other two methods by allowing you to specify what to sell to generate the highest possible tax loss. Since you hand-select which shares to sell, you can maximize your gains and manage your income for income taxes. You can sue your tax losses to offset your capital gains or up to $3,000 in ordinary income.

Understand the drawbacks. The process of selecting specific shares to sell and calculating the cost basis and capital gains and losses is not automated. It involves a lot of record-keeping. You need to keep track of all of your purchased assets and any adjustments to the cost, including stock splits, commissions and any other transactions. In addition, you need to keep accurate records of the sale of the assets in order to calculate the capital gains or losses.

Tracking Your Cost Basis

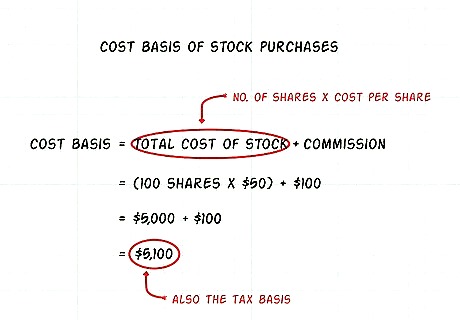

Track the cost basis of stock purchases. You need to adjust the cost basis of stock purchases for any commission you pay to a broker. You add this to the original cost. The total cost of the stock plus the commission equals the tax basis. For example, suppose you purchased 100 shares at $50 per share and you paid a $100 commission. The cost basis is (100 x $50) + $100 = $5,000 + $100 = $5,100.

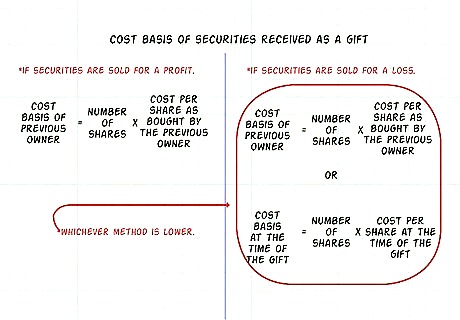

Determine the cost basis of securities you receive as a gift. If you sell the securities for a profit, the cost basis equals the cost basis of the previous owner. If you sell the securities for a loss, you can use either the cost basis of the previous owner or the value of the stock at the time of the gift, whichever is lower. You have to use the lower value because you cannot write off losses that happened before you owned the securities.

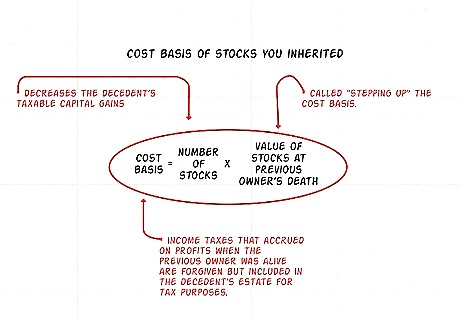

Establish the cost basis of stocks you inherit. When you inherit stocks, the cost basis is the value of the stocks at the time of the previous owner’s death. This is called “stepping up” the cost basis, and it assumes that the value of the stock has increased over time. Stepping up the cost basis benefits the person who inherited the stock because it decreases their taxable capital gains. Any income taxes that accrued on profits when the previous owner was alive are forgiven but included in the decedent's estate for tax purposes.

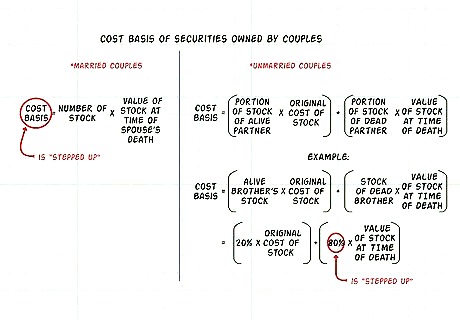

Track the cost basis of securities owned by married couples. If your spouse dies, the cost basis of any stocks is stepped up to the value of the stocks at the time of the death. It is almost like you inherited the stock. If unmarried couples own stock together, the portion of the cost basis that gets stepped up when one dies is determined by the portion owned by the other person. For example, suppose two brothers purchase stock together. One contributed 80 percent and the other contributed 20 percent. If the brother who contributed 80 percent dies, the cost basis of 80 percent of the stock would be stepped up to the price at the date of death.

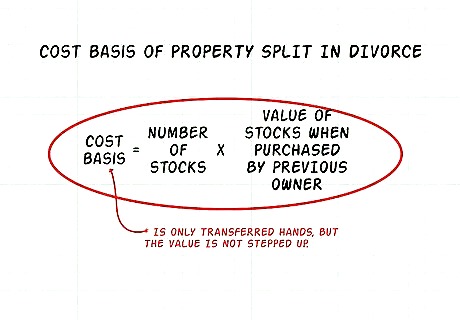

Determine the cost basis of property split in a divorce. If assets are transferred from one person to another in a divorce, the cost basis also changes hands. This means that the cost basis is not stepped up. The amount of the cost basis for the new owner equals the cost basis of the previous owner.

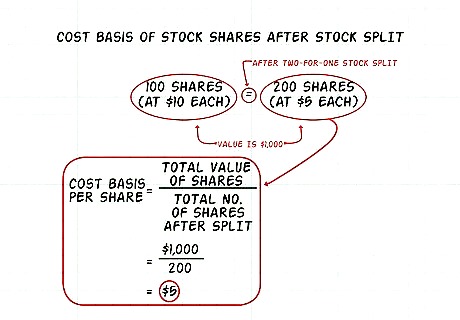

Track cost basis after stock splits. If you own stock shares in a company and the company splits the stock, your cost basis is spread evenly across the old and new shares. For example, suppose you own 100 shares of $10 stocks for a cost basis of $1,000. The company declares a two-for-one split, so now you own 200 shares of stock, but the cost basis remains $1,000. The only thing that changes is the cost basis per share, which now equals $5 ($1,000 / 200 = $5).

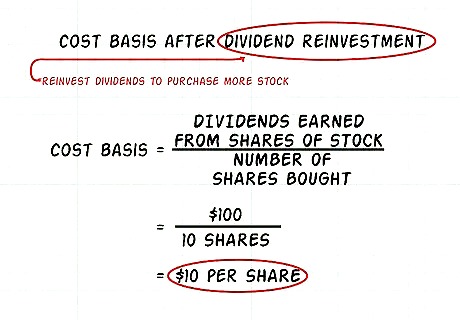

Track your cost basis after dividend reinvestment. If you sell some stock, you may choose to reinvest those dividends to purchase more stock. This is called dividend reinvestment. Suppose you made $100 from dividends on your shares of a stock, and you reinvested that to purchase 10 more shares of stock. The cost basis for each of those shares of stock is $10 ($100 / 10 = $10).

Comments

0 comment